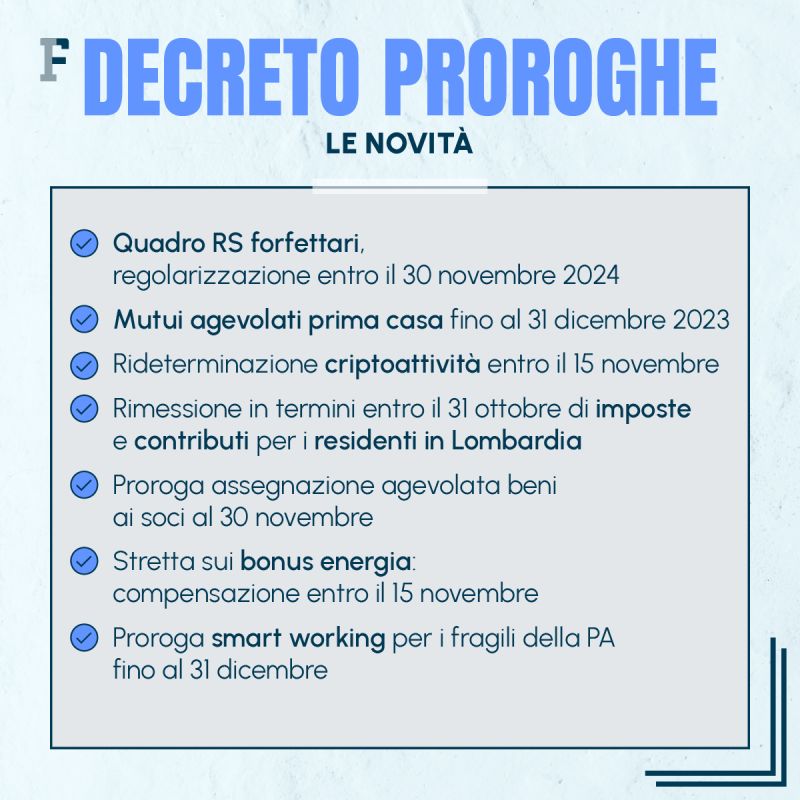

There is no rush to settle the tax return for taxpayers with a fixed VAT number: extension of sending the supplementary return, there will be time until November 30, 2024

the Fixed rate system Also included in the discussion of the extension decree: the deadline has been postponed to November 30, 2024 to submit a file Supplementary statement Necessary to address any errors and/or omissions.

It is up to notification Invitation messages for spontaneous adaptation Addressed to thousands of Flat rate taxpayers It has attracted the attention of sector operators at all levels.

Surrounding wave of controversy Fill out Part RS of the tax return It started from the bottom and reached representatives of institutions.

as I expected Deputy Minister of Economy and Finance Maurizio Liu, heresy It’s important to come up with Extension decree Which will be discussed in the Council of Ministers today, September 27.

There is talk of the rule being postponed to 2024Commitment to communicating data provided under RS.

Interested readers can receive free updates on tax, financial, and employment information via email Subscribe to our newsletter for freeone free update per day via email Monday through Sunday at 1 p.m

Messages to fixed-wage workers Is the RS framework correct or does it not exist? News coming soon about the settlement

There will be time for settlement until November 30, 2024.

This is the news that emerges from the extension decree. So, there’s another year to plan what to do and send out the supplementary announcement without haste.

Beyond heresy On the Organizing the tax return Provided for the 2021 tax period, it is worth analyzing i Possible cases And instructions provided by the revenue agency.

The form assembly is considered correct

In this case, the same message that the revenue agency sent to taxpayers provides a flat rate Instructions to follow:

“If you believe that you are not required to report these data in Form RS, which must be filled out by taxpayers applying the flat rate system for those carrying out business, arts and professions activities, we invite you not to take this letter into account”

So there is no PEC or in any case no explanation: simple as that “Archive/Trash” Incoming message.

Form assembly not found

In this case too, the sent message suggests Solution:

However, if he believes our reports are correct, he can His regularity across the Active repentance (Article 13 of Legislative Decree No. 472/1997) Benefiting from reduced penalties. In this case, you will have to file a supplementary return and pay a fee A fine of 250 euros (Paragraph 1 of Article 8 of Legislative Decree No. 471/97), to be reduced according to the timing of the settlement.”

In this case it is necessary to proceed Submit the supplementary declaration Which contains missing data withApplication of active repentance And pay the fine “Reduced depending on settlement timing.”.

applicationRepentance Institute any Legislative Decree dated 12/18/1997 n. 472 In the case in question the following may apply Discounts:

- 1/8 of the minimum by November 30, 2023;

- 1/7 of the minimum by November 30, 2024;

- 1/6 of the minimum after November 30, 2024.

Fixed price compliance letters: ways to regulate the RS framework

It is possible, but not appropriate, except in rare cases where there are other concurrent violations that need to be addressed, for an application Institutes “rare” served with Budget Law 2023.

It was also assumed that the so-called private repentance, the institution mentioned in paragraph 174, could be applied:

“With reference to taxes administered by the Revenue Agency, offenses other than those determinable under paragraphs 153 to 159 and 166 to 173 may be committed, in relation to properly filed returns relating to the tax period current on 31 December 2021 and previous tax periods, regulating the payment of eight One-tenth of the legal minimum penalties that can be legally imposed, plus tax and interest due.”.

As an exception to the ordinary order of active repentance, it gives possibility Regulating incorrect statements That is, barring last-minute extensions, by October 2, a particularly attractive date Reducing the penalty As shown at 1/18 of the applicable minimum.

But from the writer’s point of view, its application seems a gamble in view of this Absence or incorrect information Supplied with RS frame Doesn’t affect Calculate taxes due But at most it can be considered an element that can affectVerification and control activities for financial management.

Institute seems more important Correcting formal violations Referred to in Paragraph 166 of the 2023 Budget Law:

“166. Violations, violations and non-compliance with obligations or obligations of an official nature that are not related Determine the tax base For income tax purposes, value added tax and regional tax on productive activities can be regulated and paid by: Pay an amount equal to 200 euros For each tax period indicated by the violations.

An important step is noted to orient yourself between the rules Circular No. 2/H 2023 issued by the Revenue Corporation:

“Anyway, it is pointed out Failure to comply with formalities and obligations that is likely to hamper monitoring activities, even if it is only possible; Otherwise, this would constitute “only formal” violations, to which Article 6 of the Legislative Decree of December 18, 1997, No. 472, states, in paragraph 5 bis (introduced under Article 7, paragraph 1, letter a), of the Legislative Decree of January 26, 2001, No. (Chapter 32), non-punishment, because these violations do not affect the determination of the tax base, the tax, or the payment of the tax, and do not prejudice the supervisory activity carried out by the financial administration (see Circular No. 32). August 3, 2001, No. 77/H).

For example, but not limited to, specific violations include:

- Submission of annual returns prepared in a manner inconsistent with the approved forms, or incorrect indication or incomplete data relating to the taxpayer (see Article 8, paragraph 1, of Legislative Decree of December 18, 1997, No. 471); ”

The example seems appropriate to the case in question, and hence it is clearly in the absence And other formal violations To be processed for the same tax year, failure to send daily fee data considered for the purposes of settling the taxes due, the application of this institution is considered confirmed More difficult than normal repentance.

Messages to fixed-wage workers: There is no rush to organize, the news comes with the extension decree

In light of the above and in view of prior news about the timing RS frame regulation Coming from Deputy Minister Liu, in the writer’s opinion there is no need to do so Race to repentance by November 30 In order not to lose the reduction to 1/8 or even less, proceed with the reduction to 1/18 stipulated in the 2023 Budget Law, fixing everything in a hurry and perhaps making other mistakes in the rush to close everything. Next Monday.

Shannon Bailey writes for Hardwood Paroxysm, covering news, politics, business, technology, sport, entertainment, and lifestyle. They focus on clear reporting, current affairs, and stories that matter to readers, providing reliable information in an accessible and engaging way.